What are rising interest rates doing to our credit card debt? In 7 charts.

Credit Cards: spending less yet paying more

The simplest explanation for increasing interest rates during a period of high inflation, economists tell us, is to curtail purchasing and not add fuel to ever-higher prices. Of course, the interest rate set by the Federal Reserve applies to the largest borrowers, but as we all know, it quickly transfers to consumer markets, cranking up all the rates that are tied to it. One of those is the interest rate charged on credit card balances that carry over month-to-month. So, how does this strategy affect consumers?

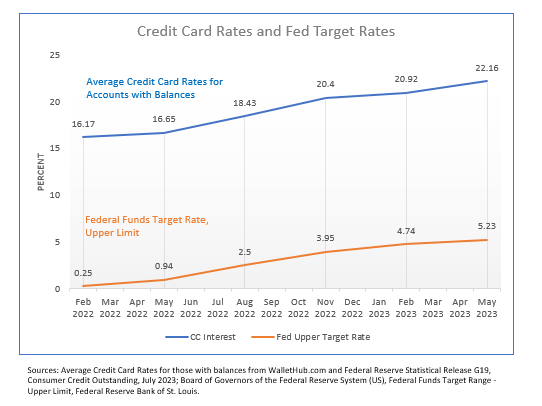

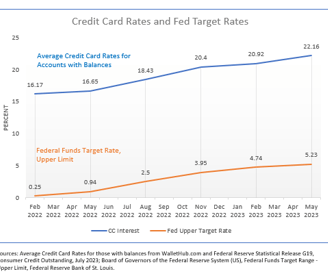

Credit card rates rise

The average consumer credit card rate on accounts that accrue finance charges rose almost six full percentage points between February 2022 and May 2023, a difference of about $5 per $1,000, give or take some rounding. In June, the Federal Reserve rate increased to 5.25%. It was hiked again in July to 5.5%, the highest since 2001.

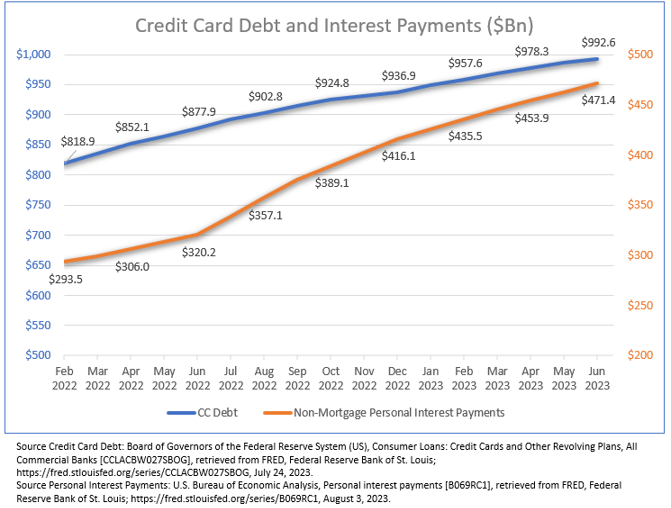

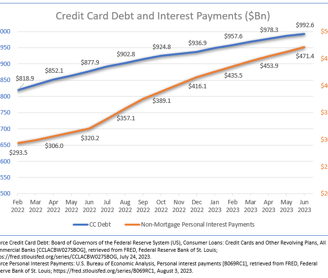

Debt piles up

By June 2023, consumer credit card debt topped $992 billion, an increase of 21%, or $173.7 billion, in 17 months.

Interest Payments increase

During that time, non-mortgage personal interest payments, measured by the U.S. Bureau of Economic Analysis, grew 60%.

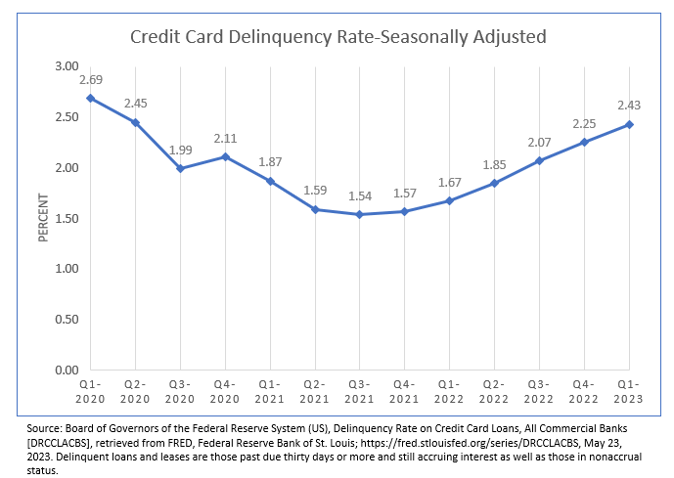

Meanwhile, credit card delinquency is on the rise

As interest payments grew, credit card delinquency rates continued to tick up to 2.43% in the first quarter of 2023. According to Transunion, the delinquency rate on unsecured personal loans, which includes student loans and discretionary loans, was even higher for Q1 2023, reaching 3.91%.

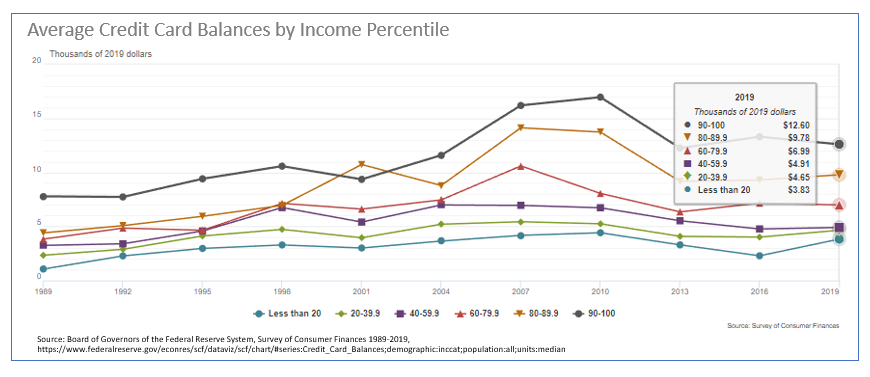

Lower-income, less debt but a higher DTI

Although credit card delinquency was climbing, it did not mean that lower-income groups were most susceptible. In fact, it could be the opposite since the credit limit and total debt for lower-income groups are significantly below those of higher-income segments.

Generally, credit card spending in actual dollars is highest among higher-income groups. As an example, in 2019, the average credit card debt of the 90%-to-100% income percentile was $12,600. It was about a third of that for the lowest income groups: $3,830. However, those at the bottom rungs usually pay a higher percentage of their income toward that debt. Annuity.org calculated this in 2021 as 26.1% for the lowest-income earners and 4.3% for the highest.

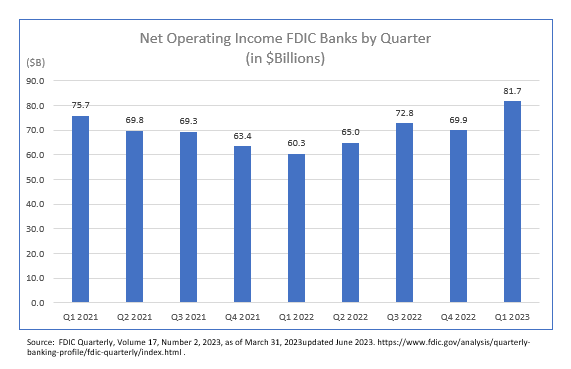

Banks are doing pretty well, though

While consumers were paying more interest on past purchases, the banks seemed to be doing OK. Although many factors contribute to the net operating income of a bank, including seasonality, the balance sheets of FDIC-insured banks recorded a strong first quarter in 2023.

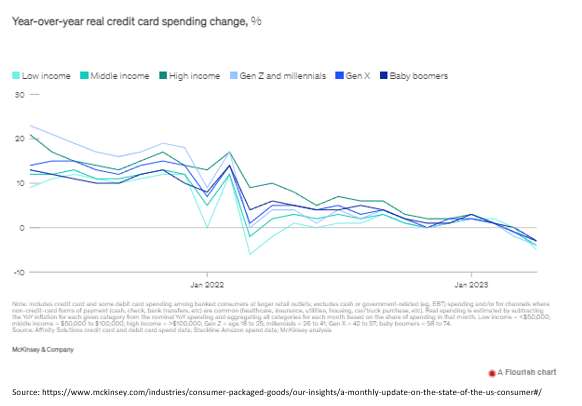

Consumer spending (via credit cards) is down

So, are higher interest payments and inflation driving down consumer spending? According to McKinsey’s June 2023 Monthly Update on the State of the Consumer, all income groups have reduced their credit and bank card transactions since January, but lower-income groups (designated as an income of less than $50,000 per year) have decreased their purchases most.

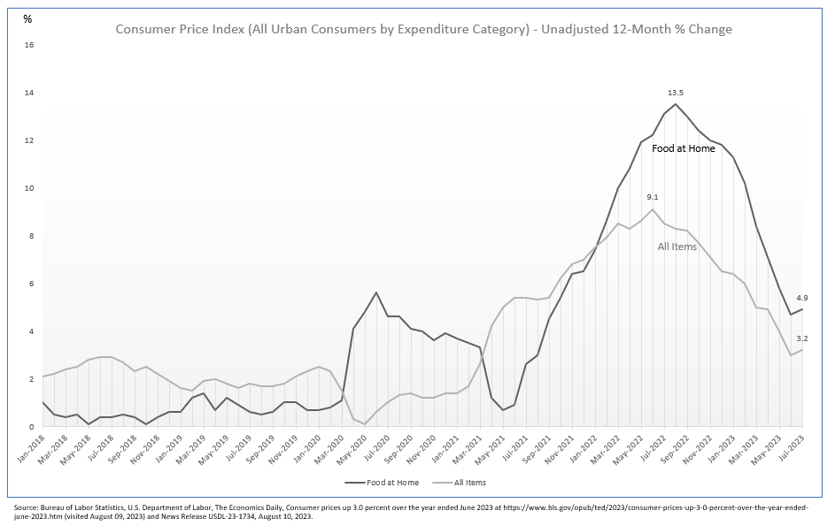

Is inflation down?

Yes, inflation is down. Reduced spending can boost supplies and lower prices; however, using the consumer pocketbook as a cudgel to chip away at inflation seems particularly cruel. This is especially so in light of stagnant wages, high home prices, and elevated consumer prices on everyday items such as food, which show a stubborn resistance to fall in line.

Tags: market research, analytics, economy, inflation, credit cards, credit card debt, food prices, Fed, Federal Reserve